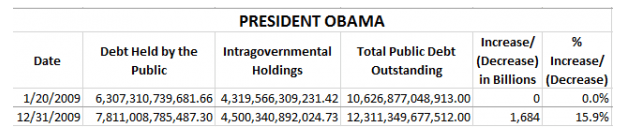

I am not an authority on economics. I am, however, a person who watches what goes on around me and sometimes learns lessons from what I see. Some economic principles are obvious enough to be learned that way.

In 2013, Forbes Magazine posted an article quoting a statement by then-President Obama on the subject of economic freedom. Economic freedom was not something President Obama believed in. President Obama acted on his belief that economic freedom was not a good thing, and the American economy suffered during his presidency.

The article quotes a speech President Obama gave in Kansas:

there is a certain crowd in Washington who, for the last few decades, have said, let’s respond to this economic challenge with the same old tune. “The market will take care of everything,” they tell us. If we just cut more regulations and cut more taxes–especially for the wealthy–our economy will grow stronger. Sure, they say, there will be winners and losers. But if the winners do really well, then jobs and prosperity will eventually trickle down to everybody else. And, they argue, even if prosperity doesn’t trickle down, well, that’s the price of liberty.

Now, it’s a simple theory. And we have to admit, it’s one that speaks to our rugged individualism and our healthy skepticism of too much government. That’s in America’s DNA. And that theory fits well on a bumper sticker. (Laughter.) But here’s the problem: It doesn’t work. It has never worked. (Applause.) It didn’t work when it was tried in the decade before the Great Depression. It’s not what led to the incredible postwar booms of the ’50s and ’60s. And it didn’t work when we tried it during the last decade. (Applause.) I mean, understand, it’s not as if we haven’t tried this theory.

Well, have we tried this theory? A little history is in order here.

The article reminds us:

I pick 100 years deliberately, because it was exactly 100 years ago that a gigantic anti-capitalist measure was put into effect: the Federal Reserve System. For 100 years, government, not the free market, has controlled money and banking. How’s that worked out? How’s the value of the dollar held up since 1913? Is it worth one-fiftieth of its value then or only one one-hundredth? You be the judge. How did the dollar hold up over the 100 years before this government take-over of money and banking? It actually gained slightly in value.

Laissez-faire hasn’t existed since the Sherman Antitrust Act of 1890. That was the first of a plethora of government crimes against the free market.

…Obama absurdly suggests that timid, half-hearted, compromisers, like George W. Bush, installed laissez-faire capitalism–on the grounds that they tinkered with one or two regulations (Glass-Steagall) and marginal tax rates–while blanking out the fact that under the Bush administration, government spending ballooned, growing much faster than under Clinton, and 50,000 new regulations were added to the Federal Register.

The philosophy of individualism and the politics of laissez-faire would mean government spending of about one-tenth its present level. It would also mean an end to all regulatory agencies: no SEC, FDA, NLRB, FAA, OSHA, EPA, FTC, ATF, CFTC, FHA, FCC–to name just some of the better known of the 430 agencies listed in the federal register.

Even you, dear reader, are probably wondering how on earth anyone could challenge things like Social Security, government schools, and the FDA. But that’s not the point. The point is: these statist, anti-capitalist programs exist and have existed for about a century. The point is: Obama is pretending that the Progressive Era, the New Deal, and the Great Society were repealed, so that he can blame the financial crisis on capitalism. He’s pretending that George Bush was George Washington.

Please follow the link to read the entire article. It accidentally explains the reasons the economy has prospered under President Trump. I also strongly recommend reading The Creature From Jekyll Island by G. Edward Griffin for the story behind the creation of the Federal Reserve System.